Unpacking a DTC Use Case: GLP-1s

Some business models behind the boom

On February 21, 2025, the FDA declared an end to GLP-1 shortages. How will pharmaceutical and DTC telehealth companies adapt? Will they pivot, co-exist, and/or find new ways to operate?

For the past several years, GLP-1s have dominated the digital health discourse. As the market has evolved, multiple go-to-market strategies for the provision of GLP-1s have emerged, each offering a distinct route for consumers considering or seeking these medications. This article explores several business models influenced by market and regulatory forces.

The 4 Main GTMs (that I’ve observed)

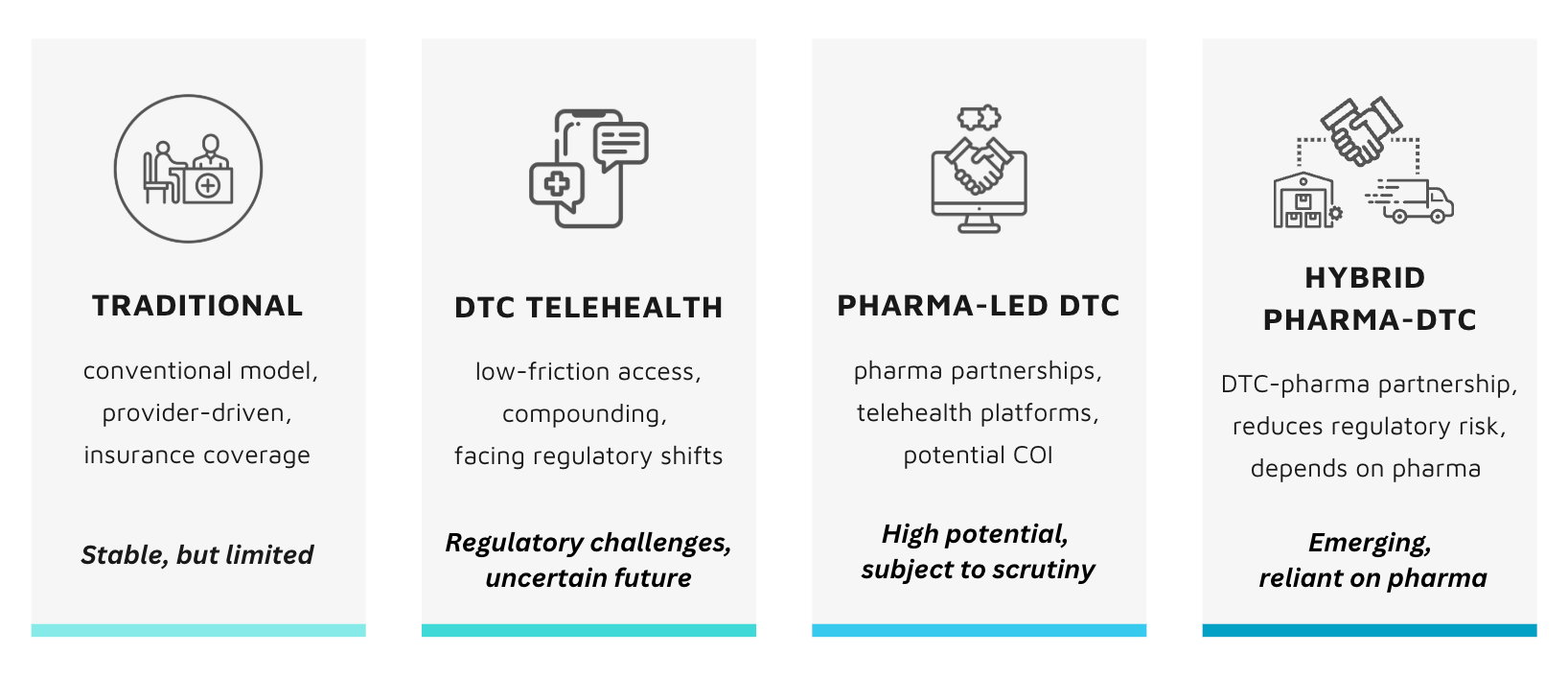

Model 1: Traditional provider-to-pharmacy route

This is the conventional pathway through which most GLP-1 prescriptions are accessed. In a traditional provider-to-pharmacy route, a patient sees a healthcare provider (either in-person or via telehealth), the provider evaluates the clinical appropriateness, and (if deemed necessary) prescribes the medication. The patient picks up the medication at a pharmacy or has it delivered to their home.

Here, the patient first interacts with a provider, not a prescription-focused platform. This route usually relies on insurance coverage and prior authorization processes. The medications obtained through this model are FDA-approved and adhere to established safety standards.

Things to consider:

Cost barriers: Patients may face challenges in accessing GLP-1 prescriptions due to variability in insurance coverage, copays, and prior authorization requirements.

Provider-related barriers: Patients might not have a provider they can consult, while some providers may be reluctant to prescribe GLP-1s.

Model 2: DTC telehealth model

In this model, consumers engage directly with DTC telehealth platforms, typically completing a short questionnaire, having a “streamlined” provider interaction, and receiving a prescription. This minimal friction model is cash-pay and sometimes structured as a subscription service. Well-known players using this model include Hims & Hers, Ro, and Noom.

In the case of GLP-1s, these companies have largely relied on compounding pharmacies to fill an access gap during the drug shortages and offer lower-cost alternatives. If you’ve been following this space, you know the ins-and-outs of compounding but here is a quick summary. Compounding pharmacies are not a novel development. They serve critical functions in the pharmaceutical ecosystem, such as customizing formulations for patients who require modifications. These include allergy adjustments, alternative delivery mechanisms (e.g., liquid formulations for children who cannot swallow pills), and access to medications during FDA-declared shortages.

In light of the GLP-1 shortages, compounding pharmacies were able to produce compounded semaglutide, and DTC telehealth platforms partnered with these pharmacies for procurement. However, compounded medications also come with complications: they don’t go through the same FDA-approval processes as commercially manufactured drugs, meaning variability in safety and quality is possible (here’s one notable example of compounding gone wrong).

While compounding has been essential for GLP-1 distribution, its role is now fundamentally changing, forcing DTC telehealth companies that built a business around compounding to pivot. Certainly these players knew this shortage was going to come to an end. Big question here is: how will they adapt?

From recent messaging from some companies, it seems like “personalization” will be one approach. Notably, this is happening amid increased scrutiny around compounding following the Hims & Hers Super Bowl ad, which raised questions about pharmaceutical marketing of platforms offering compounded drugs.

Things to consider:

Regulatory dependency: With the FDA declaring the Novo Nordisk GLP-1 shortages are over, DTC companies will no longer be able to sell compounded versions of semaglutide after the 60 to 90 day transition period. Moving forward, compounded formulations must be meaningfully different to comply with regulations (I smell AI).

Sustainability: A business strategy dependent on shortages is not sustainable. Unfortunately, consumers are the ones who will bear the brunt of this transition.

Consumer understanding: Consumers may not fully understand the difference between compounded medications and FDA-approved GLP-1s. With compounded semaglutide now taken out of the checkout cart, questions about access and quality will likely arise. The industry must ensure informed decision-making isn’t sacrificed for unruly access.

Interestingly, the news of the end of the shortage occurred on Friday, so we saw the market slightly react re the Hims stock, but I’m very curious to see what Wall Street thinks this week, following Hims’ earnings call on Monday.

Model 3: Pharma-led DTC model

Pharmaceutical engagement with consumers has primarily been via marketing, but over the past year, we’ve seen a shift to pharmaceutical companies experimenting with their own DTC platforms. This approach involves a partnership between pharmaceutical companies and telehealth vendors. Under this model, consumers visit a pharma-branded DTC platform, such as LillyDirect, where they are routed to visit a provider through a partner telehealth platform. From there, providers can assess clinical appropriateness. This model seems to centralize the prescription-seeking journey through the manufacturer’s ecosystem. There are some potential ethical issues with this model, particularly regarding conflicts of interest. Some senators have questioned a few of the players in this space; in response, companies have pushed back, stating that providers on partnered platforms are not influenced to prescribe their drugs.

[The experimentation of pharma companies with DTC partnerships is a trend that deserves its own piece!]

Things to consider:

Ethical concerns: When pharmaceutical companies control the patient entry point for prescription access, it raises concerns about potential conflicts of interest in prescribing behavior.

Regulatory tension: I don’t think we’ve seen the end of scrutiny from regulators about how these platforms operate.

Model 4: Hybrid pharma-DTC model

There’s a subtle difference between this model and the pharma-led DTC approach, and the key distinction lies at the gateway of consumer-initiation. In a hybrid model, the consumer visits the platform of a DTC telehealth player that has partnered with a pharmaceutical manufacturer. For example, in December 2024, Ro announced a partnership with LillyDirect, allowing consumers to access Zepbound vials through Ro. Previously, these vials were only available via LillyDirect, so this partnership marks an expansion of the drug’s availability though DTC channels.

I’m quite intrigued by this model. DTC telehealth companies source from pharma rather than compounding pharmacies, mitigating some regulatory scrutiny. Pharma companies avoid risks of overextending their reach into the sale of medications. The pricing strategy might favor consumers.

Things to consider:

Market uncertainty: This model is new (barely three months old!). Whether this model can scale is an open question.

Sustainability: DTC companies will likely depend on pharma’s willingness to maintain this partnership. If there is a restriction of availability, then these platforms would lose access.

Final thoughts

The GLP-1 market has been a case study in regulatory arbitrage, supply-and-demand forces, and real-time business model pivots–like changing a tire while the car is moving. 2024 was a year of experimentation with different strategies being tested. 2025 will likely be a year of reckoning, where we find out which models can scale, survive regulatory pressures, meet consumer expectations, and of course, deliver high-quality care.

The one thing that I feel is certain: the direct-to-consumer model is here to stay. But what “DTC” means in this space and how it manifests and evolves is very much TBD.

Let me know how you’re thinking about this space. What do you envisage in the future of GLP-1s?